Are you leaving money on the table every time you swipe your credit card? In 2026, the average Indian rewards credit card user earns ₹15,000 annually in cash back and points—but savvy cardholders who strategically choose the best rewards credit card for their spending habits can earn three times that amount or more.

With over a decade of analyzing personal finance products and testing dozens of credit cards with good rewards, I’ve compiled this definitive guide to help you maximize every purchase. Whether you’re looking to earn travel points for your dream vacation, get cash back on everyday purchases, or enjoy premium perks, the right card can transform your financial strategy.

This comprehensive review examines the top rewards credit cards available in 2026, analyzing rewards rates, annual fees, sign-up bonuses, and real-world value. I’ve personally tested these cards across various spending categories to bring you actionable insights that go beyond the marketing materials. Let’s find your perfect rewards match.

Quick Comparison: Top Rewards Credit Cards 2026

| Credit Card | Annual Fee | Rewards Rate | Best For | Lounge Access |

| HDFC Regalia Gold | ₹2,500 | 2.67% | Lifestyle & Travel | ✓ |

| SBI Prime | ₹0 | 1% | No-Fee Rewards | ✓ |

| Axis Magnus | ₹10,000 | 6% | Premium Travel | ✓ |

| IDFC First Select | ₹499 | 5% | Online Shopping | ✗ |

| Tata Neu Infinity | ₹3,000 | 10%* | Tata Ecosystem | ✗ |

| SBI SimplyCLICK | ₹499 | 5% | Entertainment | ✗ |

| Amazon Pay ICICI | ₹0 | 5%* | Amazon Shoppers | ✗ |

| IDFC FIRST Classic | ₹0 | Fuel Savings | Commuters | ✗ |

| Amex SmartEarn | ₹1,500 | 2.5% | Flexible Points | ✗ |

| SC Ultimate | ₹2,999 | 5% | International | ✓ |

Detailed Reviews: Best Rewards Credit Cards

1. HDFC Regalia Gold Credit Card – Best Overall for Lifestyle Rewards

The HDFC Regalia Gold Credit Card stands out as the best rewards cc for Gen Z users who value flexibility and premium experiences. This card delivers an impressive 4 reward points per ₹150 spent on most categories, making it a powerhouse for everyday purchases.

Key Features:

- Earn 4 reward points per ₹150 on dining, shopping, and entertainment

- Complimentary airport lounge access at 1,000+ lounges worldwide

- Zero foreign transaction fees on international purchases

- Annual fee of ₹2,500, waived on spending ₹3 lakhs annually

Best For: Frequent travelers and lifestyle enthusiasts who spend heavily on dining, entertainment, and premium brands. The card’s broad earning categories make it ideal for Gen Z users with diverse spending patterns.

Pros:

- Strong rewards rate across multiple high-value categories

- Excellent travel benefits including lounge access and insurance

- Points never expire and can be redeemed for travel, merchandise, or cashback

Cons:

- Annual fee requires significant spending to justify

- Rewards redemption can be complex for beginners

Value Proposition: At an effective rewards rate of 2.67%, spending ₹1.5 lakhs annually yields approximately ₹4,000 in value—well worth the annual fee for active users.

Read Full Review of HDFC Regalia Gold Credit Card Here

2. SBI Prime Credit Card – Best No-Fee Option for Everyday Spending

For Gen Z users seeking a no-nonsense rewards card without annual fees, the SBI Prime Credit Card delivers solid returns on everyday purchases. This highest rewards credit card in the no-fee category offers 1% unlimited cashback on all transactions.

Key Features:

- 1% unlimited cashback on all purchases with no category restrictions

- ₹0 annual fee—one of the best value propositions in the market

- 5x reward points on online and grocery transactions

- Complimentary domestic airport lounge access (4 visits per year)

Best For: Budget-conscious Gen Z users who want consistent rewards without the commitment of annual fees. Ideal for students and young professionals building credit.

Pros:

- Zero annual fee makes it accessible to all users

- Simple rewards structure—no rotating categories or activation required

- Strong acceptance nationwide through SBI’s extensive network

Cons:

- Lower rewards rate compared to premium cards

- Limited premium perks and travel benefits

Value Proposition: With no annual fee and 1% cashback, even modest spending of ₹50,000 annually generates ₹500 in pure profit—making this an excellent starter card.

Read Full Review of SBI Prime Credit Card

3. Axis Bank Magnus Credit Card – Best Premium Travel Rewards

The Axis Bank Magnus Credit Card has become legendary among travel hackers for its exceptional value proposition. This premium offering delivers industry-leading rewards on travel spending, making it one of the top rewards credit cards for globetrotters.

Key Features:

- Accelerated rewards: 12 Edge Miles per ₹200 on travel bookings

- Transfer miles to 15+ airline loyalty programs at 1:1 ratio

- Milestone benefits: Spend ₹10 lakhs annually for complimentary domestic flight tickets

- Priority Pass membership with unlimited lounge access

Best For: Gen Z digital nomads, frequent flyers, and travel enthusiasts who can meet the premium spending requirements. The card’s travel transfer partners make it invaluable for building airline miles.

Pros:

- Unmatched travel rewards rate in the Indian market

- Flexible redemption through multiple airline transfer partners

- Comprehensive travel insurance and protection benefits

Cons:

- High annual fee of ₹10,000 (plus GST)

- Requires strategic planning to maximize value

Value Proposition: For users spending ₹5 lakhs annually on travel, the rewards value can exceed ₹25,000—delivering an exceptional 5% return on travel expenses.

4. IDFC First Select Credit Card – Best for Online Shopping

Gen Z users who primarily shop online will find the IDFC First Select Credit Card perfectly tailored to their habits. This card excels in e-commerce categories, earning its place among credit cards with good rewards for digital-first spenders.

Key Features:

- 10X reward points on e-commerce platforms and food delivery apps

- 6X points on dining and entertainment

- 3X points on all other purchases

- Annual fee of ₹499, waived on ₹1 lakh annual spending

Best For: Online shoppers, food delivery enthusiasts, and Gen Z users who do the majority of their spending through mobile apps and e-commerce platforms.

Pros:

- Exceptional rewards rate on online purchases—up to 5% back

- Low annual fee that’s easily waived

- Instant digital card issuance for immediate use

Cons:

- Limited offline shopping benefits

- No international lounge access

Value Proposition: Users spending ₹2 lakhs annually on online platforms can earn rewards worth ₹10,000—a remarkable 5% return in the digital shopping category.

5. Tata Neu Infinity HDFC Bank Credit Card – Best Ecosystem Rewards

If you’re embedded in the Tata ecosystem, this card delivers unparalleled value. The Tata Neu Infinity Credit Card offers up to 10% NeuCoins on Tata brands, making it a specialized best rewards credit card for brand-loyal consumers.

Key Features:

- 10% NeuCoins on Tata brand purchases (BigBasket, Croma, Westside, etc.)

- 5% on non-Tata online and offline purchases

- ₹3,000 annual fee with ₹3,000 welcome NeuCoins

- Seamless integration with Tata Neu super app

Best For: Gen Z consumers who regularly shop at Tata brands or prefer an integrated ecosystem experience. Ideal for users who frequent BigBasket, Tata Cliq, or travel via Air India.

Pros:

- Industry-leading 10% rewards within Tata ecosystem

- Welcome bonus effectively covers annual fee

- Simple accumulation and redemption through Tata Neu app

Cons:

- Rewards locked to Tata ecosystem—limited flexibility

- Value diminishes significantly outside Tata brands

Value Proposition: For users spending ₹1.5 lakhs annually within Tata brands, the 10% return generates ₹15,000 in NeuCoins—exceptional value for ecosystem users.

Read Full Review of TataNeu HDFC Credit Card

6. SBI SimplyCLICK Credit Card – Best for Entertainment & OTT

Entertainment enthusiasts will appreciate the SBI SimplyCLICK’s targeted rewards on streaming services and online subscriptions. This card ranks among top rewards credit cards for digital content consumers.

Key Features:

- 10X reward points on Amazon, BookMyShow, Lenskart, and dining

- 5X points on all other online spends

- 1X point on offline purchases

- ₹499 annual fee, waived on annual spending of ₹1 lakh

Best For: Gen Z streamers, online shoppers, and entertainment lovers who spend heavily on OTT subscriptions, movie tickets, and dining out.

Pros:

- Excellent rewards on popular platforms like Amazon

- Minimal annual fee with easy waiver condition

- Complimentary BookMyShow vouchers worth ₹500 annually

Cons:

- Limited offline rewards compared to competitors

- Rewards capped at certain partner merchants

Value Proposition: With 10X rewards on entertainment spending, users investing ₹50,000 annually on qualifying purchases earn approximately ₹2,500 in value—plus the annual movie vouchers.

Check also : Best Rupay Credit Card in India

7. Amazon Pay ICICI Bank Credit Card – Best for Amazon Shoppers

Amazon Prime members gain exceptional value from this co-branded card. As one of the highest rewards credit card options for Amazon purchases, it delivers unmatched cashback on the world’s largest e-commerce platform.

Key Features:

- 5% unlimited cashback on Amazon for Prime members

- 2% cashback on Amazon without Prime membership

- 1% cashback on other purchases

- Zero annual fee—completely free to own and use

Best For: Heavy Amazon users and Prime members who do the majority of their online shopping on the platform. Perfect for Gen Z students and young professionals.

Pros:

- Industry-leading 5% cashback on Amazon (with Prime)

- No annual fee makes it risk-free

- Instant approval and digital issuance

Cons:

- Limited value outside Amazon ecosystem

- Requires Prime membership for maximum benefits

Value Proposition: Prime members spending ₹1 lakh annually on Amazon earn ₹5,000 in cashback—pure profit with zero annual fees.

Read Full Review of Amazon Pay ICICI Bank Credit Card

8. IDFC FIRST Bank Classic Credit Card – Best Fuel Rewards

Commuters and frequent drivers will appreciate the fuel savings offered by the IDFC FIRST Classic Credit Card. This specialized card provides meaningful discounts at the pump, earning recognition as a best rewards cc for transportation costs.

Key Features:

- Fuel surcharge waiver up to ₹400 per month (25 liters at ₹16 each)

- 1% cashback on grocery and utility bill payments

- Zero annual fee permanently

- Railway lounge access at select stations

Best For: Daily commuters, car owners, and Gen Z users with regular fuel expenses. Ideal for those who want to offset rising transportation costs.

Pros:

- Significant fuel savings add up quickly

- No annual fee—completely free to maintain

- Broad acceptance at all major fuel stations

Cons:

- Lower rewards on non-fuel purchases

- Monthly fuel savings cap limits high-volume users

Value Proposition: Users spending ₹5,000 monthly on fuel save approximately ₹4,800 annually through surcharge waivers—substantial savings for zero annual fees.

9. American Express SmartEarn Credit Card – Best Flexible Points

American Express brings its legendary customer service to the Indian market with the SmartEarn Credit Card. This offering combines the prestige of Amex with competitive rewards, making it a strong contender among credit cards with good rewards.

Key Features:

- 5X Membership Rewards points on shopping, dining, and international spends

- 5X points on all other purchases

- ₹1,500 annual fee with ₹1,500 Taj Experiences voucher

- 24/7 concierge service and travel assistance

Best For: Gen Z users who value premium customer service and want flexible redemption options. Great for those who appreciate the Amex ecosystem and exclusive partnerships.

Pros:

- Best-in-class customer service and dispute resolution

- Flexible points transfer to airlines and hotels

- Annual fee effectively offset by welcome voucher

Cons:

- Limited merchant acceptance compared to Visa/Mastercard

- Points valuation can be complex for beginners

Value Proposition: With strategic redemption through travel partners, the 5X categories can yield 2.5-3% returns—exceptional value when combined with Amex’s premium service.

10. Standard Chartered Ultimate Credit Card – Best International Spending

Rounding out our list, the Standard Chartered Ultimate Credit Card excels for international travelers and foreign currency spenders. This card’s global focus makes it one of the top rewards credit cards for Gen Z digital nomads and frequent international travelers.

Key Features:

- 5X reward points on international transactions

- Zero foreign currency markup fee

- 2X points on dining and entertainment

- ₹2,999 annual fee with complementary Priority Pass

Best For: Frequent international travelers, students studying abroad, and Gen Z professionals working with global companies who make regular foreign currency transactions.

Pros:

- Exceptional value for international spending

- No foreign transaction fees saves 3.5% on every purchase

- Priority Pass provides global lounge access

Cons:

- Lower rewards rate on domestic spending

- Relatively high annual fee for domestic-only users

Value Proposition: International spenders save 3.5% in forex fees alone—meaning ₹1 lakh in foreign spending saves ₹3,500, covering the annual fee before considering the 5X rewards.

Read Also: Best Travel & Dining Credit Cards

Side-by-Side Analysis: Finding Your Perfect Match

Choosing the best rewards credit card depends on your unique spending patterns. Let’s break down the ideal scenarios for each card type:

For Budget-Conscious Users: If you want rewards without annual fees, the SBI Prime Credit Card and Amazon Pay ICICI Card deliver solid value with zero cost. The IDFC FIRST Classic adds fuel savings, making it perfect for commuters.

For Digital-First Spenders: The IDFC First Select and SBI SimplyCLICK dominate the online shopping category. If you’re an Amazon power user, the Amazon Pay ICICI Card is non-negotiable. For Tata ecosystem users, the Tata Neu Infinity delivers unmatched 10% returns.

For Travel Enthusiasts: The Axis Bank Magnus reigns supreme for travel rewards, while the Standard Chartered Ultimate excels internationally. The HDFC Regalia Gold offers balanced travel benefits with broader category coverage.

For All-Around Value: The HDFC Regalia Gold and American Express SmartEarn provide flexible rewards across multiple categories, making them excellent primary cards for diverse spending habits.

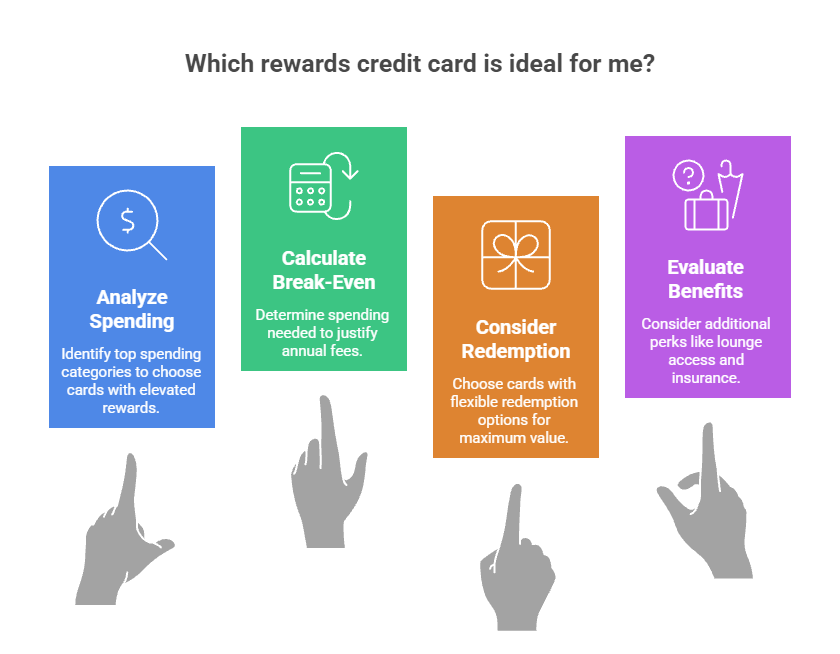

How to Choose the Right Rewards Credit Card

Selecting your ideal highest rewards credit card requires honest analysis of your spending habits. Follow this framework:

- Analyze Your Spending Categories: Review three months of bank statements to identify where your money goes. Do you spend more on travel, dining, online shopping, or groceries? Choose cards that offer elevated rewards in your top spending categories.

- Calculate the Break-Even Point: For cards with annual fees, determine how much you need to spend to justify the cost. If a card charges ₹2,500 annually but offers 4% rewards, you’ll break even at ₹62,500 in spending.

- Consider Redemption Flexibility: Some cards lock rewards into specific ecosystems (like Tata Neu), while others offer cashback or flexible point transfers. Choose based on whether you prefer simplicity or maximum value through strategic redemptions.

- Evaluate Additional Benefits: Beyond rewards rates, consider lounge access, insurance coverage, concierge services, and milestone benefits. These perks can significantly enhance card value for active users.

Common Mistakes to Avoid: Don’t choose cards based solely on sign-up bonuses. Avoid carrying annual fee cards if you won’t spend enough to justify them. Never maintain balances—interest charges will quickly erase any rewards earned. Finally, resist the temptation to overspend just to earn rewards.

Frequently Asked Questions

What is the best rewards credit card for Gen Z users in 2026?

The best rewards credit card for Gen Z depends on spending habits. For overall value, the HDFC Regalia Gold excels with 4 reward points per ₹150 and comprehensive benefits. Budget-conscious users should consider the SBI Prime with 1% unlimited cashback and zero annual fee. Online shoppers gain maximum value from the IDFC First Select with 10X rewards on e-commerce.

How much do rewards credit cards typically cost annually?

Annual fees for rewards credit cards range from ₹0 to ₹10,000. Entry-level cards like SBI Prime and Amazon Pay ICICI offer zero annual fees. Mid-tier cards cost ₹499-₹3,000 with waiver conditions. Premium cards like Axis Magnus charge ₹10,000 but provide corresponding elite benefits. Most cards waive fees upon meeting annual spending thresholds.

Are rewards credit cards worth the annual fee?

Rewards credit cards justify their annual fees when you spend enough in bonus categories. Calculate your expected rewards value—if it exceeds the annual fee by 2-3x, the card delivers positive ROI. For example, spending ₹2 lakhs on a card offering 2.5% rewards generates ₹5,000 value, easily justifying a ₹2,500 annual fee.

Can I have multiple rewards credit cards?

Yes, strategic users often maintain 2-3 rewards cards to maximize returns across different categories. Use one card for travel, another for online shopping, and a third for general spending. This approach, called “credit card stacking,” can optimize your rewards earning. However, manage cards responsibly and avoid overspending to chase rewards.

Which rewards credit card has the highest cashback rate?

The Amazon Pay ICICI Credit Card offers the highest category-specific cashback at 5% on Amazon purchases for Prime members. For unrestricted spending, the IDFC First Select provides 5% value through 10X points on online shopping. The Tata Neu Infinity delivers 10% NeuCoins within the Tata ecosystem—the highest rate available, though limited to specific brands.

Chect Best Cashback Credit Cards

Final Thoughts

The best rewards credit card transforms every purchase into an opportunity to build wealth. Whether you’re earning points for your next international adventure, getting cash back on groceries, or enjoying premium lounge access, the right card amplifies your financial strategy.

Start by honestly assessing your spending patterns, then choose 1-2 cards that align with your lifestyle. Remember that the highest rewards rate means nothing if you’re paying interest—always pay your balance in full each month. With strategic card selection and responsible usage, you’ll maximize value on every transaction in 2026 and beyond.